Scam reimbursement is a hot topic among regulators worldwide. Here’s a summary across countries:

US – While unauthorized electronic fraud is well-covered under Regulation E, there’s no mandatory reimbursement for scams where users are tricked into sending money. Barring the state of California, where there are regulations to protect elders, offering elder protections even if the victim gave consent, there are no wider laws protecting from scams. In 2024, under CFPB pressure, P2P payments platform Zelle voluntarily began refunding victims of certain imposter scams (where someone impersonates a trusted contact), though this isn’t legally mandated. Recently, CNBC reported that 19% of Zelle scam claims at the top 3 US banks (38.6M out of 206.8M) were paid.

UK – The UK leads scam reimbursement reforms. Since October 2024, for Authorized Push Payment (APP) scams, banks using the Faster Payments system must refund victims within 5 days, deducting £100, and capping payouts at £85,000. Reimbursement is shared 50:50 between sender and receiver banks. Exemptions exist for gross negligence, delayed reports, or victim collusion.

Australia – The approach is more preventive rather than compensatory, emphasizing compliance with a Scam Prevention Framework rather than prescribing refunds. Marking a departure from the UK model, this framework covers a wider range of payment types and cuts across multiple sectors as well.

New Zealand – NZ in my view, uses a hybrid model, blending UK and Australian practices. The NZBA has introduced new consumer protections being phased in this year. If banks fail to meet five new anti-scam commitments, they’re expected to compensate eligible customers wholly or partially for scam losses depending on both the bank meeting commitments and the customer’s response.

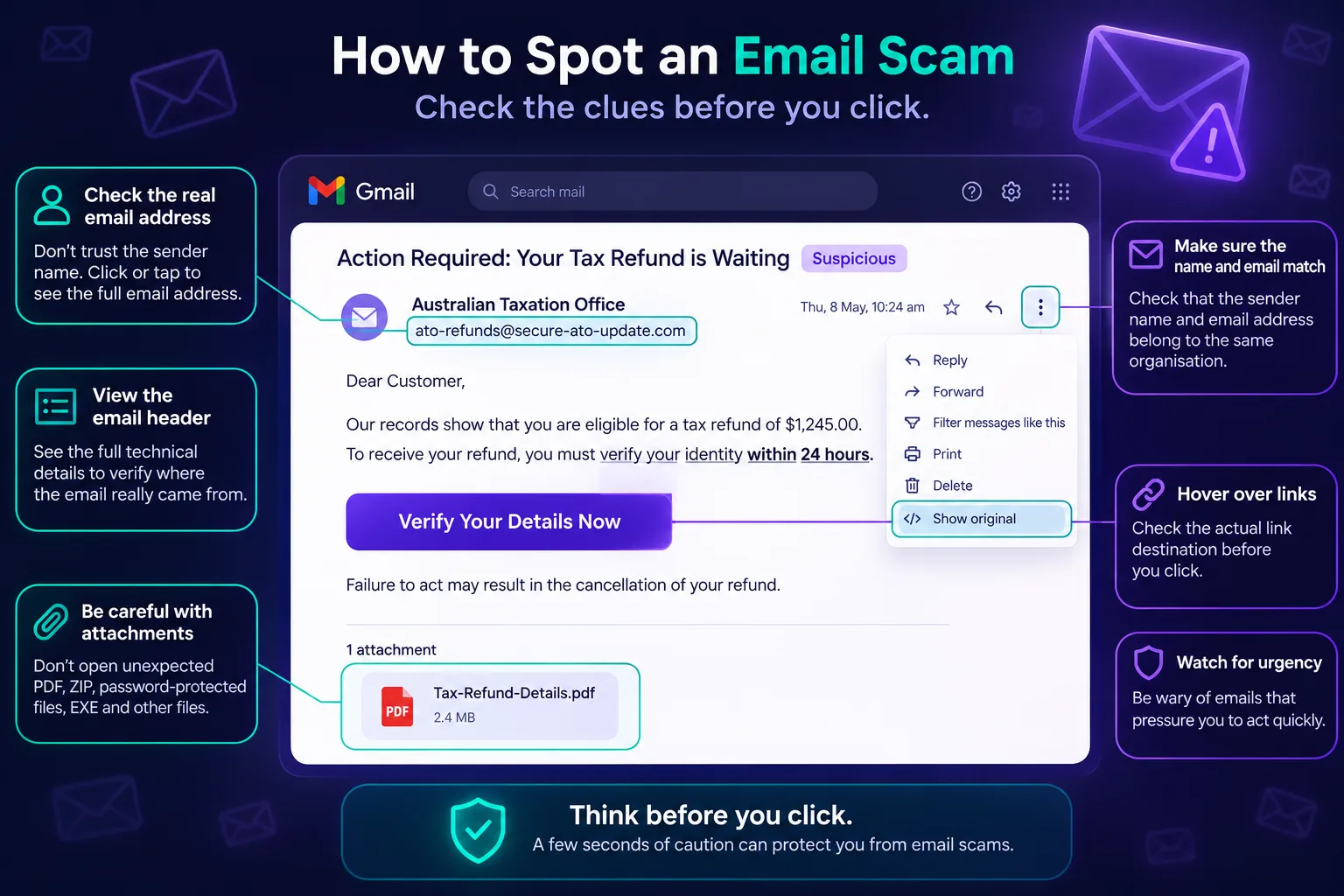

India – Here, there is an eerie silence on the topic of scam reimbursements. Any sign of user involvement and the burden fully falls on the victim. HDFC bank recently entered the global top 10 banks by market cap, joining US and Chinese giants. We need strong banks, I get it. But what good are strong banks to the customer who’s lost his shirt. Victims eat all the losses from increasing cyber crimes. See graph.

India urgently needs a formal policy for scam refunds. Citizens who’ve paid taxes for decades are losing their life savings to a moment’s lapse of judgment. Only a few lucky ones win relief via consumer courts or the ombudsman channel. Are banks doing everything possible to prevent scams? If not, shouldn’t we re-balance this burden?

I propose a simple thumb rule:

If a citizen has paid over ₹X lakh in cumulative taxes, they should get a 50% reimbursement on scam losses capped by taxes paid. This would:

- Reward tax-compliant citizens (less than 3% of the population anyway),

- Penalize tax evaders,

- Protect legitimate saving from complete erosion,

- Incentivize banks to invest in scam defences, and

- Capping at 50% reduces risks of moral hazard.